A Life Settlement is the sale of an existing life insurance policy to a third party for a lump sum payment, which is more than its cash surrender value but less than its net death benefit.

There are countless scenarios that might encourage a policyholder to exit a life insurance arrangement. Insurance companies mainly offer their customers two choices: lapse or surrender. If the policy lapses, then the contract becomes null and void and the customer loses all amounts of premium paid over the life of the policy. If the customer chooses to surrender the policy, then the payout may be as little as 3-5% of the policy’s face value.

As Americans enter their senior years, they often experience unexpected changes that cause them to reevaluate their priorities. Policies that once made sense for them, may no longer be appropriate under new circumstances. For instance, decisions that seemed appropriate when policyholders had dependent children may no longer seem appropriate once the children are grown and have moved on. Quality improvements in insurance policies over the years are driving individuals to abandon policies they consider to be outdated.

The example below illustrates a typical scenario of how a life settlement benefits a seller. For a $950,000 policy face value, a policy with a cash surrender value of only $52,000. However, for the same policy (if sold on the secondary market in a life settlement transaction), would have a $236,000 settlement price which provides 4x the cash surrender value:

There are a variety of situations in which a policyholder might wish to sell his or her life insurance policy:

- The premiums on the policy are no longer affordable.

- The beneficiary for whom the policy was originally purchased is now deceased or no longer has a need for the policy.

- A key-man policy, designed to protect a company from the financial loss of a key executive, is no longer necessary, either because the business has folded or the individual is no longer integral to the business’s success.

- The policyholder owns multiple life insurance policies and wishes to eliminate one.

- The policyholder wishes to replace an individual policy with a survivorship policy, a long-term care insurance policy, or funds for long-term care.

- The policyholder requires funds to pay for medical expenses or for new and experimental treatments for himself or someone close to him.

- The sale of the policy would allow the policyholder to maintain a desired standard of living and live out his or her final years with dignity.

- An increase in the liquidity of the policyholder’s estate eliminates the need for the policy.

A life settlement is an option for a growing number of policy owners. Policy owners are free to sell and transfer ownership of their policies, rather than continuing to pay premiums on a policy that no longer serves its original purpose or surrendering the policy for a low cash value.

According to a recently published report, “Empirical Investigation of Life Settlements“, policy owners who settled (sold) their policies from 2001 to 2011 received 404% more cash than surrendering their policy back to the life insurance company. Unquestionably, life settlements offer a rational and profitable exit strategy that addresses the financial objectives of policyholders.

While we believe fractional life settlements are a great investment opportunity and have a lot of potential upside for our investors, this opportunity may not be suitable for all investors. Before investing with us or any other life settlement investment, please consult a trusted adviser and make sure this investment class fits into your overall investment risk tolerance and timeline.

Please see some additional resources for investing with us and rules specific to California life settlement investing guidelines:

California SB 1837 (Q exemption)

| View California Life Settlement Guidelines Here |

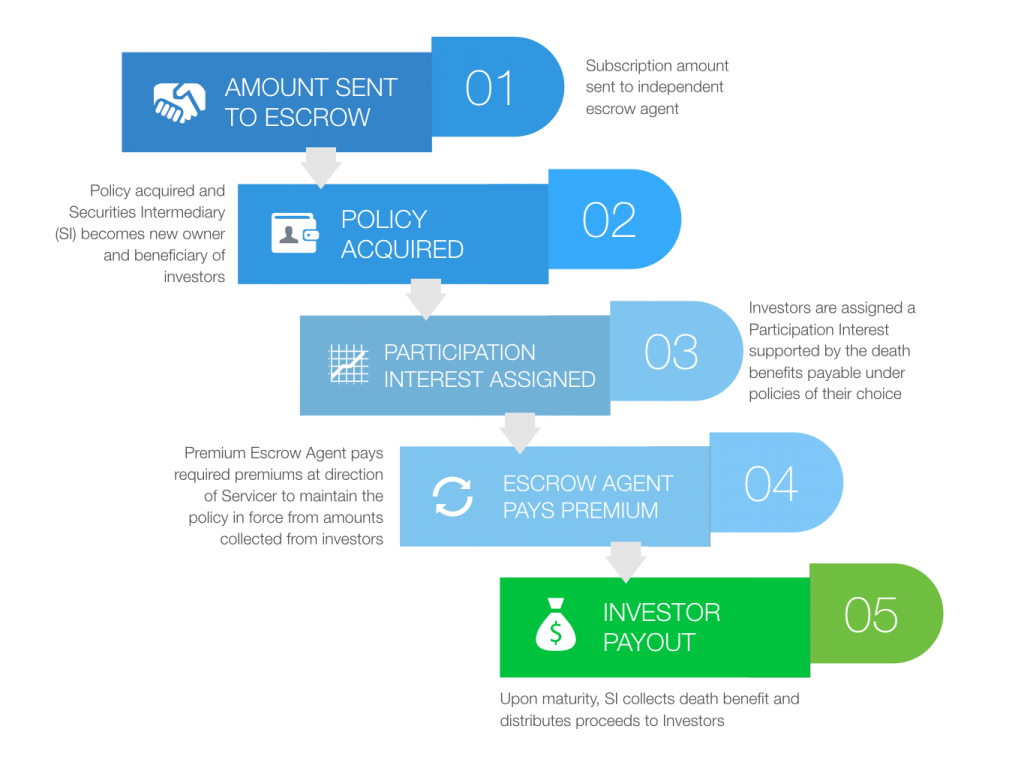

How It Works

- Qualified CA investors review SPG’s offering materials with their advisor to ensure an investment in PolicyShares™ is suitable for their investment objectives.

- Subscription Agreement is completed and the investment funds are sent to escrow agent.

- Polices are identified and presented to investors for consideration. Investor chooses the policy that backs his or her Participation Interest and the policy is acquired from investor funds.

- Investor receives from SPG a Participation Interest Certificate to evidence the policy whose death benefit supports the investor’s Participation Interest.

- Policy Servicer oversees billing and payment of ongoing premiums from the premium escrow account and tracks life insured until maturity of policy.

Selection For Our Investors

The PolicyShares™ strategy is designed to offer California (qualified) investors entry into an investment asset class widely utilized by big banks, hedge funds, pensions, and even Warren Buffet of Berkshire Hathaway.

PolicyShares™ allows an investor to acquire from SPG a Participation Interest in a portion of a life insurance policy. The Participation Interest gives the investors the right to receive from a third party beneficiary a portion of the death benefit payable under a specific policy once paid to that beneficiary by the life insurance company that issued the policy. Our investors have the option to invest in a Participation Interest relating to a single policy or multiple policies. We truly believe our platform is structured to offer unmatched flexibility in design.

Experience Our Investors Can Trust

There are 3 pivotal aspects to consider when contemplating investing in life settlements. Get these right and you have the potential for double digit returns and predictable gains. It is SPG’s experience and knowledge that makes it one of the leading life settlement company’s in California.

- Policy Acquisition and Due Diligence

Our management team has a combined 20 years of experience in the life settlement industry and policy acquisition, and our investors can know that SPG will search out strong policies in the market.

- Life Expectancy Underwriting

SPG will utilize LE reports from the same firms the big institutional investors use. Our policies are priced correctly because they are underwritten correctly!

- Servicing the Policy After Investing

When you invest with Select Policy Group, you relax knowing our company has the experience and knowledge to make sure the policies you invest in are tracked and serviced all the way through payout. With nearly 20 years of servicing life settlement transactions from our affiliated companies we have an unmatched track record for our investors.